Forming an LLC is not the only choice, as businesses might choose to form a corporation or other type of business entity. One needs to realise that forming an LLC is a procedure that provides personal liability protection as well as a formal business structure. So, if for some reason they find themselves contemplating whether or not to form an LLC, then ask this one question: “Why exactly does this business need an LLC?”.

At this point, factors influencing their decision probably include the question of how will they be personally affected? What does the process entail? and, what the tax implications are? After they have taken all of this into consideration, there are many benefits of forming an LLC that become apparent. These advantages include being protected against lawsuits, less paperwork compared to those of corporations and other legal entities, no double-taxation, a more credible business structure to both customers and creditors, flexibility, and protection of assets.

This aside they also need to familiarise themselves with different business structures. For every small business, this is by far the most important consideration. When choosing between legal business structure types the following needs to be taken into account:

- What will the profit and risk level be?

- Is being investor-friendly important?

- Would maintaining a complex business structure be worth the effort and expense?

Deciding on a business structure is guided on whether or not the business will require personal liability protection. “This will ensure that the business owner will not be held personally accountable for the event of the business suffering a loss.”So according to llcguys.com — forming an LLC is the best solution to limit your liability as a private person.

What are the different business structures?

The Informal Business Structures which do not offer personal liability protection.

Informal business structures do not offer taxation benefits or even personal liabilityprotection. They are classified under two forms of structures:

Sole proprietorship- refers to a business owned by an individual that is notnecessarily formally structured. As a sole proprietor, an individual need to file taxesunder his or her name and is held personally liable for any actions taken againstthe business.

General partnership – refers to a business that is owned by more than one individual

and the business is more formally structured. Taxes are filed under the names of the

partners and partners are also liable for any action taken against the business.

The utilization of Informal Business Structure is best suited for a business with the

following characteristic:

- The business needs to possess a low chance of liability or financial loss.

- The customer base of these business structures are usually smaller (often extended to friends, family and neighbours).

The second business structure is the Formal Business Structure which does not offer personal liability protection. Formal business structures do offer taxation benefits, as well as increased credibility, and most importantly, personal liability protection. They are classified under two forms of structures:

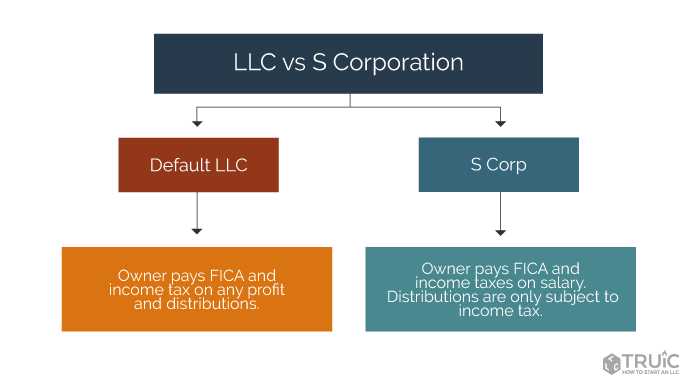

Limited Liability Company (LLC) – refers to a formal legal business structure and is owned by its members. Utilizing an LLC is the simplest form of structuring a business to protect the assets in the event of the business suffering a loss. This structure also offers distinctive tax benefits.

Corporation – refers to a formal legal business structure that is owned by shareholders. A corporation offers personal liability protection, however, it is more complex to maintain than an LLC. Corporations have their own set of tax benefits as well as investment opportunities.

When is an informal business structure applicable?

The utilization of Informal Business Structure is best suited for a business with the following characteristic:

- A larger customer base.

- Have the potential for immediate and sustainable profit.

- Increased risk of liability or loss.

- Stand to gain from unique tax options.

In the end, the decision is still on the business owner to make, and just like any business decision, there are advantages and disadvantages which guide the choices. Understanding the options upfront is always beneficial, knowing what the business stands to gain and lose in both the long and short term is a smart business choice. To aid the decision making process access some more useful information here.